EdTech Industry Insights 2026: Market Trends, AI & Growth

Edtech is becoming more disciplined and outcome-driven, with $2.6B invested in 2025 (+11%) as AI shifts from hype to practical, skills-focus

Remember 2021? Edtech was going to change everything. Capital flooded in, valuations soared, and it felt like every learning problem was about to get solved by an app. Then came the hangover — two years of sharp funding contractions, shutdowns, and a collective reckoning with whether any of it actually worked.

Fast forward to today, and the mood is different. Not pessimistic but realistic. The market has stabilized, money is flowing again, and a much clearer picture is emerging of what edtech can actually deliver. This piece pulls together the latest signals from across the global landscape to show where things stand and, more importantly, where the real opportunities are for teams building in this space.

Spoiler alert: we can help with your edtech project, too. But let’s review the data first.

The Market Grew Up (In a Good Way)

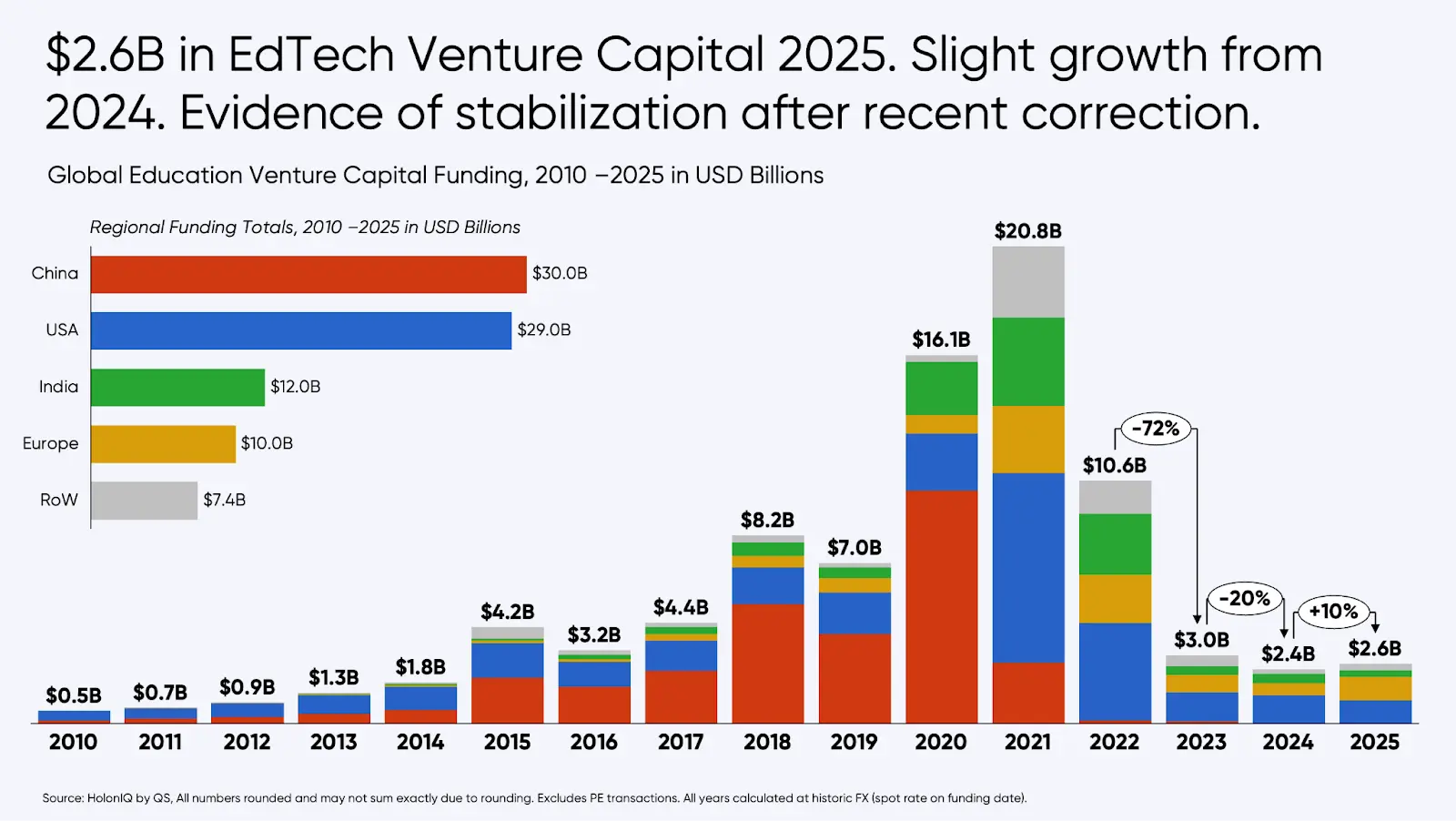

In 2025, global edtech venture investment hit $2.6 billion — up roughly 11% on 2024, according to HolonIQ. But the headline number is almost beside the point. What matters is how that money moved.

The days of throwing early-stage capital at anything with “AI” in the deck are gone. Nearly 40% of all deals in 2025 cleared the $5M threshold — a sign that investors are making bigger, more deliberate bets on companies that have already proven something. Early-stage activity held steady at around 87% of deal volume, but the quality bar rose considerably. Founders pitching in 2025 needed real demand signals, not just a compelling vision.

$2.6B global edtech VC in 2025 — up 11% on 2024 (HolonIQ)

~40% of deals exceeded $5M — capital concentrating around proven companies

The M&A story is just as telling. Around 410 transactions closed in 2025, up 20% from the year before. Two deals in particular stood out: Workday’s $1.1B acquisition of Sana, the Swedish AI-powered enterprise learning platform, and Coursera snapping up Udemy. Both deals say the same thing: AI-enabled workforce learning is no longer a niche experiment — it’s core infrastructure. This is where Unibrix comes into play with its AI services.

Who Got the Money — and Why

Workforce training dominated deal flow at 38%, with K-12 not far behind at 36% and post-secondary at 22%. The pattern reflects a sector increasingly judged on economic outcomes. Investors want to back learning that leads somewhere — a job, a promotion, a credential that employers actually recognize.

Within the “workforce,” the hot categories were cybersecurity training (Simspace pulled in $39M), AI knowledge platforms, and immersive upskilling tools. In K-12, the action was around tutoring, curriculum, and school operations — MagicSchool AI raised $45M and Starbridge raised $42M. Across both, the through-line was the same: solutions that plug into existing institutional workflows, not ones that ask schools or employers to change how they operate.

That workflow-first logic is only going to intensify in 2026. HolonIQ forecasts that capital will keep concentrating around agentic AI platforms and products with measurable, well-defined outcomes. If your product can’t show what it changes — for learners, for teachers, for institutions — it’s going to have a harder time raising.

AI Is Moving From Hype to Habit

The AI conversation in edtech has matured. A year ago, “we use AI” was enough to get a meeting. Now it barely gets you in the door. The question is: AI doing what, exactly, and what did it change?

According to HolonIQ’s 2026 Education Trends Snapshot, the AI applications that delivered real value in 2025 were unglamorous but effective:

- course design assistance,

- teacher productivity,

- administrative workflow automation,

- and targeted student support.

Not magic tutors. Not sentient learning companions. Practical tools that made people’s jobs easier and learners’ paths clearer.

One area where the AI opportunity still feels wide open: language learning. The global digital language learning market sits at around $21 billion, with a TAM estimated at $63 billion when you include offline and B2B segments. The catch? Only around 40% of that market is currently digital. The majority is still served by publishers and live instruction providers — exactly the kind of incumbents that AI-native solutions can outsmart.

Emerge, the edtech-focused VC, describes this as the third wave of digital language learning:

- there was pre-recorded content (Rosetta Stone),

- then came gamification (Duolingo),

- and now avatar-based conversational AI.

The pitch is compelling — let learners practice speaking, which is by far the most-wanted language skill, with an AI tutor at near-zero marginal cost, tailored to their level and interests. It’s one of those rare cases where the technology is genuinely ready and the market demand is clearly there.

Five Forces Shaping EdTech in 2026

HolonIQ’s 2026 snapshot highlights five shifts reshaping how institutions buy technology, how learners engage, and how EdTech companies must build.

- AI with guardrails. Institutions no longer want broad personalization promises. They want AI that is governed, auditable, and embedded into existing workflows.

- Engagement and wellbeing. As AI automates routine tasks, human factors — motivation, connection, purpose — are becoming core measures of platform value.

- Infrastructure as baseline. Shared data layers, identity management, and interoperability are no longer differentiators. Integrated platforms are expected.

- The skills economy. Specific, measurable skills are becoming more important than traditional credentials, as tools that track skills in real time along with adaptive training platforms spread across industries.

- Prove it or lose it. Education buyers increasingly demand proof that products improve outcomes — learning quality, persistence, wellbeing, or job-relevant skills.

The Nordics: A Quiet Powerhouse

If you’re building edtech and you’re not paying attention to the Nordic and Baltic region, you probably should be. HolonIQ’s 2025 Nordic Baltic EdTech 50 shows a market that’s maturing faster than most — and shifting in some interesting ways.

44% of Nordic Baltic cohort is K-12 in 2025 — lowest share ever, down from 64% in 2020

~2× growth in Workforce share since 2020 in the Nordic Baltic cohort

Finland led the 2025 cohort for the first time in five years at 26%, overtaking Sweden. Norway had its best-ever showing at 22%, with companies like Scrimba (interactive coding) and Pistachio (cybersecurity training) anchoring the list. Sweden dropped to 20% but still produced the region’s landmark deal: Sana’s $55M raise and eventual $1.1B Workday acquisition.

The B2B/D2C split tells a story too. B2B models have bounced back to 62% of the cohort — back to pre-pandemic levels after a D2C spike during COVID years. Enterprise and institutional buyers are driving growth. At the subsector level, K-12 Content & Curriculum has collapsed from 24% of the cohort in 2023 to just 9% today, while Post-Secondary Support has doubled and a brand-new Research subsector has appeared, led by Estonia’s Orvium.

For anyone building edtech software, the region is attractive for a specific reason: Nordic and Baltic clients are demanding. They care about data governance, pedagogical rigor, and measurable outcomes — which means products that succeed here tend to be genuinely good, not just well-marketed. But we’ve got a feeling we know the key to the hearts of this region.

What This Means for Builders

Three things matter most:

- Products must integrate directly into institutional workflows.

- AI must be tied to measurable outcomes.

- And learning increasingly happens on mobile.

The winners won’t build the flashiest AI. They’ll build AI that fits real systems — and proves it works. At Unibrix, we build edtech software that does exactly that.

Moombix

Kennitalan

Wooskill

technical assessment,

and project scoping.

UI/UX design, and

technical specifications.

reviews, and continuous

integration.

testing, security audits,

and bug fixes.

documentation, and

ongoing support.