Building Fintech Products in Europe After MiCA: What Actually Changed

MiCA’s grace period just ended. Here’s what fintech builders actually need to know before shipping in the EU.

On July 1, 2026, the last transitional grace period under Europe’s Markets in Crypto-Assets regulation expires. For any crypto-asset service provider operating in the EU without a MiCA authorization — regardless of how many users they serve or how long they’ve been in the market — operating now means operating illegally. ESMA has been unambiguous: there are no further extensions.

For fintech founders and product teams building anything that touches digital assets, crypto payments, stablecoins, or custody in Europe, MiCA is not a compliance item to delegate. It is a product constraint that reshapes what you can build, where you can build it, and how long it will take to get to market.

What MiCA actually requires

MiCA establishes the first unified regulatory framework for crypto-asset service providers across all 27 EU member states. Before it, a company wanting to operate across Europe navigated 27 different national regimes — with different registration requirements, different rules, and different timelines. MiCA simplifies this to a single authorization framework, though it does not replace e-money or payments law, meaning companies may still need to satisfy obligations across multiple EU regulatory frameworks simultaneously.

The scope is wide. Exchanges, custodians, wallet services, and token issuers are all in scope under MiCA — which means most fintech products that have incorporated crypto features in recent years now need to audit which license category applies to them.

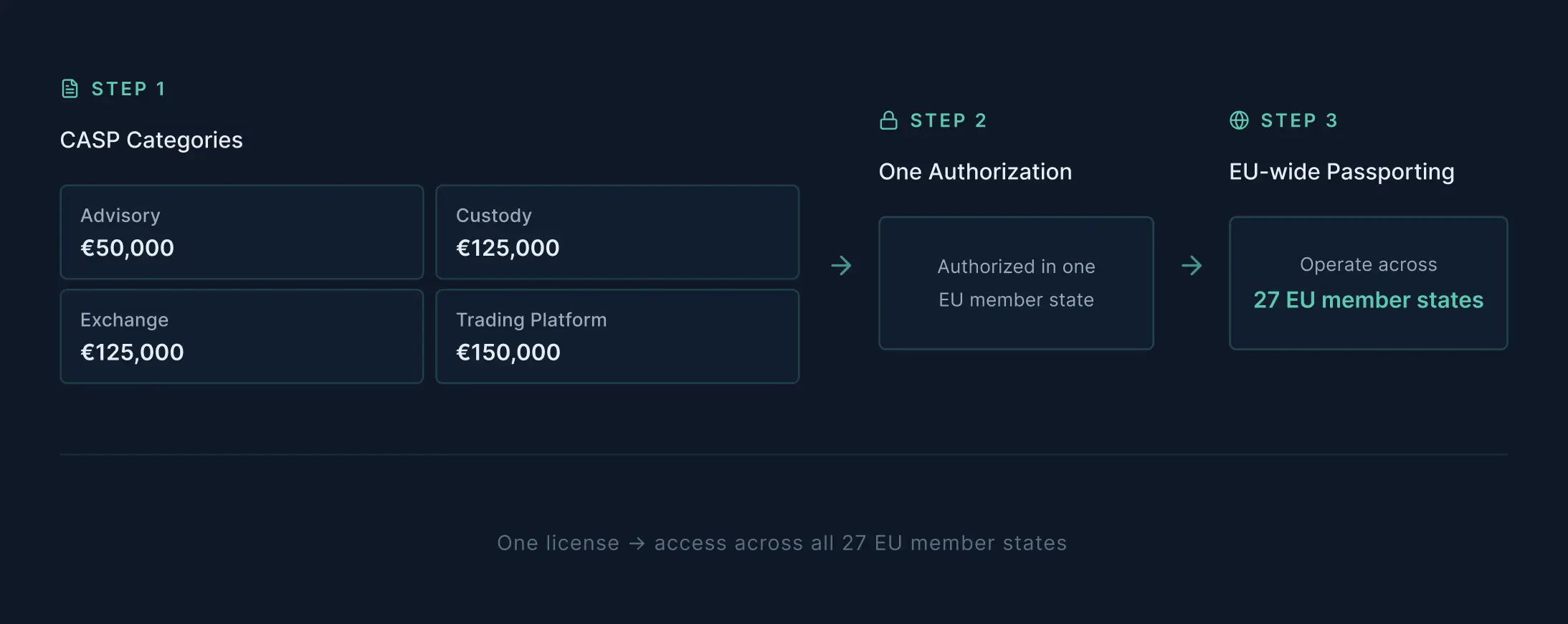

Capital requirements are real but manageable for serious operators. MiCA requires €50,000 for advisory services, €125,000 for custody and exchange services, and €150,000 for trading platforms. More significant than the capital threshold are the ongoing compliance obligations: AML/CFT processes including transaction monitoring, the Travel Rule (sender and receiver identification on every crypto transfer), governance requirements, cybersecurity standards aligned with DORA, and consumer protection disclosures.

The passporting advantage — and the jurisdiction competition

The single most consequential aspect of MiCA for product teams is passporting: a single authorization in any one EU member state gives CASPs EU-wide passporting rights — get authorized once and operate across all 27 countries. For any fintech with pan-European ambitions, this eliminates the multi-jurisdiction licensing nightmare that previously characterized EU crypto operations.

Which member state you incorporate in matters. Germany has attracted regulated banks and custodians — Commerzbank, N26, Trade Republic, BitGo; Luxembourg has been favored by global brands seeking rapid passporting, including Coinbase and Bitstamp; Malta has become a hub for large exchanges — OKX, Crypto.com, Gemini; the Netherlands moved quickly, issuing first-day approvals for payments-oriented businesses like MoonPay. Each jurisdiction has its own processing speed, interpretive approach, and strategic profile. Choosing an incorporation jurisdiction is now a product and market access decision, not just a legal one.

Transitional periods have varied dramatically — the Netherlands required compliance by July 2025, Italy by December 2025, and others extended to July 2026 — creating a period during which different rules applied in different member states simultaneously. ESMA audits in the first half of 2025 found inconsistent supervisory approaches between national authorities, identifying harmonized standards as a goal rather than a current reality.

The stablecoin problem MiCA created

MiCA’s treatment of stablecoins has had immediate market effects. Major stablecoins like USDT remain non-compliant with MiCA’s requirements for e-money token issuers, forcing exchanges to delist them and fragmenting EU liquidity. Tether has not sought MiCA authorization; Circle has, making USDC the dominant MiCA-compliant stablecoin in the EU. For fintech products building on stablecoin rails in Europe, this is not a theoretical distinction — it determines which settlement assets are legally permissible.

The dual-licensing challenge adds complexity for stablecoin products. From March 2026, electronic money token custody and transfer services may require both MiCA authorization and separate payment services licenses under PSD2, potentially doubling compliance costs and raising concerns about competitive disadvantage for EU-based stablecoin products versus offshore alternatives.

The compliance stack required

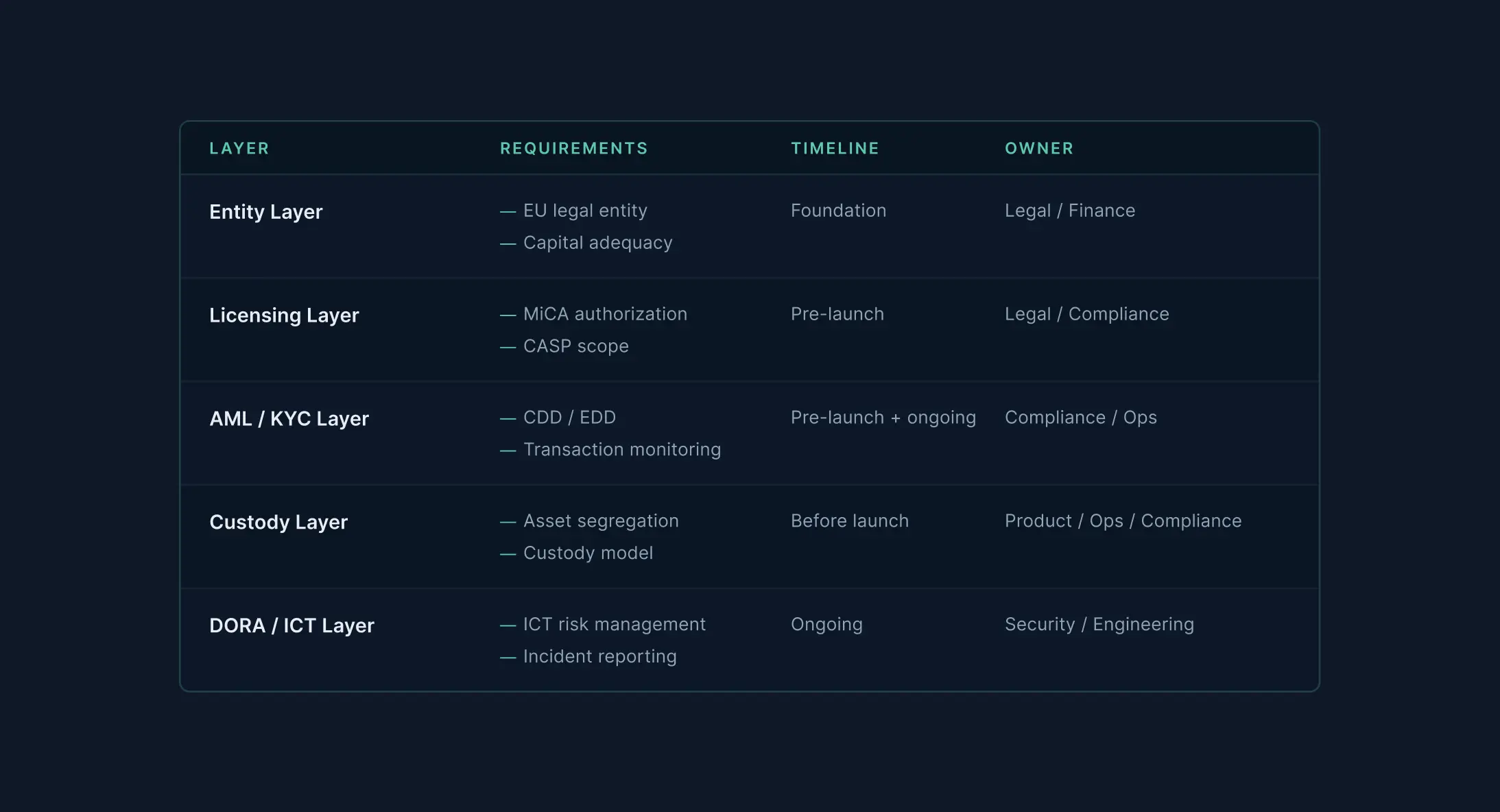

For a fintech team building a MiCA-compliant product in 2026, the compliance stack includes: a registered entity in an EU member state with appropriate capital adequacy; AML/KYC infrastructure including CDD, enhanced due diligence for high-risk profiles, and Travel Rule-compliant transaction monitoring; a custody and client asset segregation model that passes regulatory review; governance documentation; and DORA-compliant ICT risk management with incident reporting capability. With non-compliance carrying penalties of up to €5 million or 10% of annual turnover, the EU is serious about enforcement.

What the window of opportunity looks like

Authorized entities secure EU-wide passporting rights, enabling cross-border operations without 27 separate licenses. Early compliance also builds trust with institutional partners, investors, and users in an increasingly regulated environment. The companies that moved early — and there are still fewer than 50 fully licensed CASPs as of mid-2026 — have a structural advantage in institutional partnerships, banking relationships, and product distribution that slower-moving competitors cannot quickly close.

MiCA is not an obstacle to building fintech products in Europe. It is the price of entry to the world’s second-largest economy for digital asset services — and for companies that build to that standard, it is also the architecture that allows them to operate across a $1.8 trillion market without asking the same regulatory question twice.

Building a MiCA-compliant fintech product in Europe? Unibrix specializes in modular fintech systems — with expertise in HIPAA, SOC2, GDPR, and now MiCA-compliant architectures. Licensing timelines are determined by technical readiness as much as legal preparation. The right foundation changes both. → [Talk to Unibrix about your compliance architecture]

Moombix

Kennitalan

Wooskill

technical assessment,

and project scoping.

UI/UX design, and

technical specifications.

reviews, and continuous

integration.

testing, security audits,

and bug fixes.

documentation, and

ongoing support.